Temet Nosce (Know Thyself)

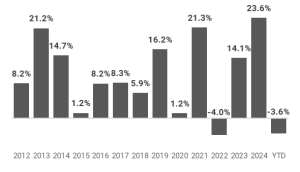

The Value Fund reached the halfway point of 2025, down -3.6% net of fees and expenses. (1) The US dollar weakened significantly and has been a drag of over -5.0% year-to-date (YTD). Here’s where the major North American market indices stand YTD: S&P500 +0.6%; DJIA -1.0%, S&P/TSX +10.2%. (2)

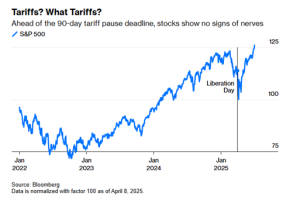

Our strong start to the year in Q1 reversed in Q2 as the markets shrugged off President Trump’s “Liberation Day” tariffs and are in full “risk on” mode.

Historically, we have been at our best when markets are at their worst. The corollary is that we struggle to keep up when markets are frothy. We see signs of excessive risk-taking in the current market: SPACs are making a comeback, stock valuations are soaring, and Bitcoin, junior gold miners, and other speculative assets are hitting new highs. A few recent headlines from The Wall Street Journal should give you a sense of the speculative nature of the current market environment:

(1) All returns and Fund details are: (a) based on Class F units; (b) net of all fees; and (c) as of June 30, 2025.

(2) Index returns are for the total return indexes, including dividends and measured in Canadian dollars, the Value Fund’s reporting currency

It won’t surprise GreensKeeper clients to learn that, given the rampant speculation, we remain cautious and patient. We have been nibbling away at a few stocks that we find interesting at current prices and trimming stocks that are trading above their fair value. Capital preservation demands no less. We have experienced similar periods like this in the past when our value investing style was out of step with the market. We take comfort in knowing that, in time, the tide will turn in our favour, as it always has.

Portfolio Update

The top contributor to the portfolio in the second quarter was American Express (AXP) +18.6%. AXP’s affluent customer base continued to spend in Q1, with revenues up 8% at constant currency, causing the stock to end the quarter just shy of its all-time high. During Q2, AXP announced upgrades to its US Consumer and Business Platinum cards, which will be released later this year. AXP continues to tailor its products to capture the spending of younger consumers, with Millennials and Gen Z now accounting for 35% of total US consumer spending. We believe these investments will strengthen the company’s network effect and further lock young consumers into AXP’s ecosystem as their incomes and card spending continue to rise. Additionally, AXP is widening its use cases on the commercial side of the business with recent product launches tailored towards working capital and expense management. This should expand the number of transactions that AXP can participate in and increase switching costs with commercial card users.

Our second-best performer in the quarter was Alphabet Inc. (GOOGL) +13.5%. During the quarter, Alphabet hosted its annual developer conference, highlighting its advancements in AI tools across its product suite. Google’s AI Overview product continues to gain traction with over 1.5 billion monthly users, and its direct ChatGPT competitor, Gemini, is now used by more than 400 million people each month. Recent updates have reinstated the company’s models to the top of the AI power rankings. Importantly for shareholders, AI Overviews have been increasing the total number of queries at Google, which the company is monetizing at a similar rate to traditional search. Google’s business fundamentals remain healthy, with operating earnings growing 20 % in Q1.

Rounding out our top 3 for the quarter was Compagnie Financière Richemont SA (CFR:SWX) +8.5%. The company’s core Jewellery Maisons (Cartier and Van Cleef & Arpels) continue to prove more durable than nearly any other luxury jewelry brand. Our original thesis—that the top branded jewelry brands would outperform the luxury sector over time—is largely playing out with Richemont’s jewelry segment growing 11% in the most recent quarter. Richemont may have a few more tricks up its sleeve. Since acquiring Italian jeweller Buccellati in 2019, sales have increased almost 5x following a strong 2025. Additionally, Richemont recently expanded its portfolio with the acquisition of another Italian jeweller, Vhernier, in June. Both brands were acquired for relatively low dollar amounts, and management continues to manage the company conservatively and for the long term. We expect strong tailwinds over the medium to long term across the luxury industry and believe Richemont remains well-positioned to capitalize on the industry’s growth.

Our worst performer in the second quarter was Fiserv (FI) -21.9%. The market reacted badly to Fiserv’s Q1 earnings release, in which it revealed that volume growth of its core Clover system was 8%, slowing from the 16% it averaged last year. The stock came under further pressure when management revealed that Clover’s business was growing at a similar pace to start Q2. Our view is that the slowdown in Clover’s growth isn’t due to a deteriorating competitive position, but due to a combination of slowing industry growth and lingering impacts from hyperinflation in some of the company’s fastest-growing markets. After recalculating our valuation for the stock, we believe the decline was overdone and added to our position throughout the quarter.

Our second-largest laggard in the quarter was Berkshire Hathaway (BRK.B/A) -8.8%. The most significant update at Berkshire was Warren Buffett’s surprise announcement that at the end of the year, he will retire as CEO, a position he has held for 60 years. It came as no surprise that Buffett will pass the torch to Canadian Greg Abel, who has been Vice Chairman of non-insurance operations for nearly a decade.

While we are saddened to see Warren stepping down as CEO (he will stay on the board as Chairman), it doesn’t fundamentally change our intrinsic value estimate of the company, and we have been assuming a pending change in leadership for many years now.

We made one new purchase in the quarter: Novo Nordisk (NVO), which we have owned previously. NVO, a Danish pharmaceutical company, is the world’s leading insulin maker. But today the company’s growth is driven by its GLP-1 franchise, which comprises Ozempic, Wegovy and Rybelsus. The stock has come under pressure following the uptake of competitor Eli Lilly’s (LLY) GLP-1 products Mounjaro and Zepbound. LLY will likely continue to gain share, but we believe the market for GLP-1s is large enough for both companies to continue increasing their revenues, and that the market is undervaluing NVO’s GLP-1 pipeline.

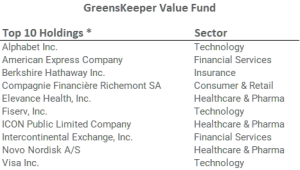

We fully exited our positions in Merck & Co. (MRK) and Vertex Pharmaceuticals Inc. (VRTX) in Q2 as both stocks were fully valued and we had better places for the capital. Our top ten holdings as of the end of Q2 are listed below.

* As of June 30, 2025. The Value Fund’s holdings are subject

to change, and are not recommendations to buy or sell any security

Market Panics

The ancient Temple of Apollo was inscribed with the maxim Temet Nosce (Know Thyself). Achieving success in investing requires reflection and being honest with oneself about how one will react when a market panic arrives.

The recent market tantrum triggered by Trump’s “Liberation Day” tariff announcements provides the perfect opportunity for self-reflection and insight into your investment temperament.

The research team at GreensKeeper used the episode to conduct a post-mortem on our actions and emotions as we navigated the pullback. We encourage you to do the same while it is still fresh in your mind.

As with most market selloffs, we received a higher-than-normal level of calls from clients who were anxious about the market’s dive. We also had conversations with several prospective clients who preferred to “wait until things settled down” before sending us their capital to manage. These are patterns that we have witnessed many times, but are counterproductive for those seeking attractive long-term equity returns.

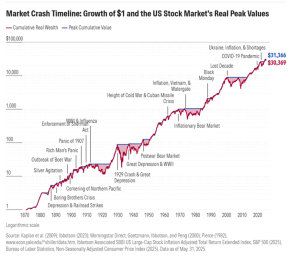

One of the (few) benefits of getting older is accumulated experience. The pullback a few months ago was the sixth major market correction our team has witnessed over its investing lifetime.(3) We think it is helpful to share some of what we have learned over the decades from these periodic market panics.

It always feels scary at the time, and one’s perspective typically narrows. Investors become convinced that the markets are going lower, as they can only see the negatives. The fear center of the brain (amygdala) takes over from the rational mind (prefrontal cortex). Fear has served a useful evolutionary purpose for our species, but it isn’t helpful when it comes to investing.

(3) While the recent Liberation Day tariff selloff wasn’t technically a correction (a >20% drawdown), it was close enough to be instructive

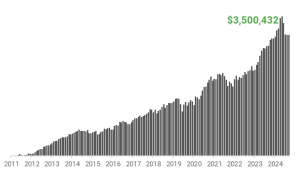

Markets inevitably recover, often quicker than one can imagine. In the case of the COVID and Liberation Day selloffs, it took just a few months (see previous table). To achieve attractive equity returns, investors cannot miss these recoveries. Investors who missed just the best 30 days of the past 25 years would have given up almost all the S&P 500’s rise (see graphic below). The reality is that investors who are fearful of entering the market become paralyzed and miss these crucial upswings. Thinking that one can time the turn is self-delusional.

Stocks are cheap when things are scariest. For the best companies in the world, that is often the only time they are on sale. In October 2008, during the depths of the Great Financial Crisis, Buffett penned an op-ed in The New York Times, stating that he was buying. He was a little early as the market didn’t bottom until the following March, but his words proved prescient:

Being aggressive by purchasing stocks when things are scary is like running towards a fire. Like first responders, it takes training and mental preparation. Overcoming one’s fear response doesn’t come naturally to most. In our experience, many people struggle to endure the emotional ups and downs of market corrections. If you are a GreensKeeper client, you have outsourced those decisions to people who can.

Our experience navigating past corrections, combined with our Stoic demeanor, gives us an edge when things get ugly. We don’t try to time when the next market correction will arrive (it can’t be done). We simply do our work in advance and with our watchlist in hand, are ready to act whenever they appear. We will move decisively, knowing that the latest market panic will be just another blip in the market’s long-term secular rise.

Firm Update

It has been an eventful quarter at GreensKeeper:

- Michael Van Loon is now registered as an Associate Portfolio Manager and continues to take on additional responsibilities at the firm.

- We had a record turnout at last month’s Annual Meeting (our 14th)! For those who were unable to join us, a video recording of the meeting is available on our YouTube channel.

- This quarterly Scorecard marks our 50th. My, how time flies.

For clients of the firm, you will receive our Half-Year Report, which includes a complete snapshot of the portfolio, in August. We are also in the final stages of launching a new client portal and implementing some new technologies. With growth comes change. Stay tuned for more details.

Enjoy the dog days of summer!

Michael P. McCloskey

President, Founder &

Chief Investment Officer